IR35

What is it?

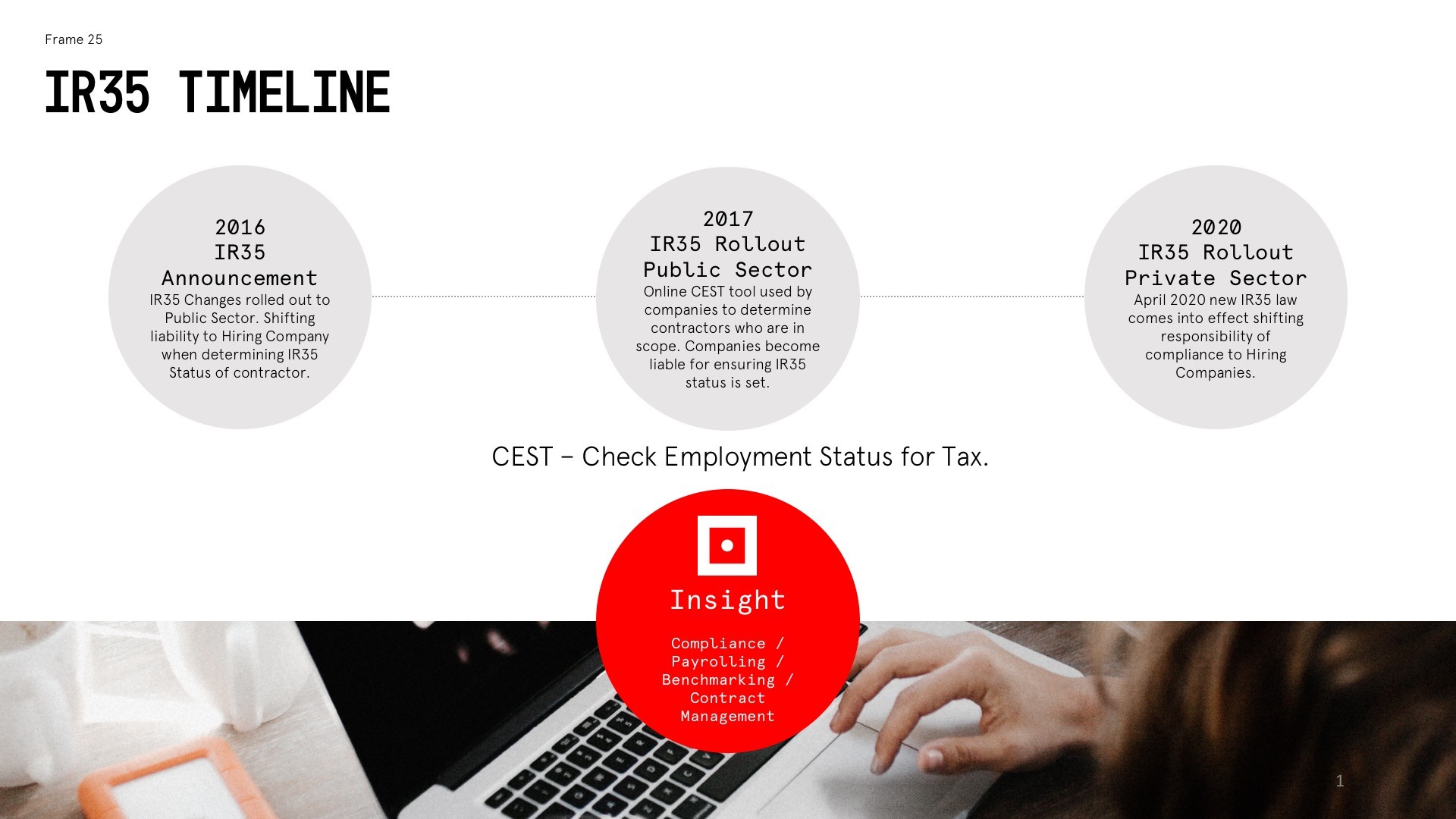

IR35 is a piece of legislation that came into force in April 2000 as an attempt by the government to curtail tax avoidance by companies paying workers ‘off-payroll’ as contractors via Personal Service Companies (PSC’s), they should have been set up as employees and subject to PAYE deductions.

The spirit behind the IR35 legislation is to do away with “disguised employees”.

Those working via a PSC as opposed to being an employee gain significant tax advantages. Likewise the engager, saves paying Employers National Insurance Contributions (NIC’s)

How is Legislation Changing?

Currently Directors of PSC’s are responsible for assessing whether the contract undertaken by their PSC is caught by the IR35 legislation.

From April 2020, the law will change the responsibility to the engager of the PSC to determine if the contract is caught by the IR35 legislation, if the engager is a large or medium sized company.

From April 2020 , if the company that engages the worker decides incorrectly that the contractor is self-employed, HMRC can investigate and insist on back payment of tax, as well as fines for late payment.

Timeline of IR35

Who is now responsible?

Engager - End Client

Fee Payer - Agency/MSP

When the public sector reforms were introduced in April 2017, the legislation introduced the concept of “fee payer” and “engager”. The engager is responsible for assessing whether IR35 applies and the fee payer liable to make any withholding due.

Where an engager pays the contractor themselves, they will be both the engager and the fee payer under the legislation. Where an intermediary is used to make payments to the contractor (e.g. an agency/MSP), it will be the entity who makes the payments that is prescribed as the fee-payer.

They will be treated as making a payment to the worker which is to be treated as earnings from an employment if the manner in which the work is undertaken means that the IR35 legislation applies. It is this fee payer who bears responsibility for accounting for the PAYE/NIC due under the IR35 legislation and the liability where any failures arise.

However, the legislation also inserted a clause which states that if an engager fails to take reasonable care in coming to its conclusion as to whether the contractor is caught by IR35 then the liability is transferred to the client.

The technical consultation on off-payroll working, released on 5 March, provides further detail on the ’transfer of debt’ provisions that may be inserted into the private sector reforms due in April 2020.

Technical consultation (5 March)

The consultation released by HMRC provides an obligation for status determinations to be passed down the labour supply chain. Should a party in the supply chain fail to pass the determination onto the next party in the chain, they will initially liable for any unpaid PAYE income tax or National Insurance Contributions (NICs) due. HMRC have also sought to extend the transfer of debt provisions, stating that if HMRC fail to collect the liability from the party that failed to pass on the determination, the liability will transfer to the first party in the supply chain (eg the MSP). Failing recovery from the first party, the liability would then ultimately transfer to the engager.

How IR35 is determined

What determines being inside?

There are a number of factors that an Engager shall consider when making a determination these include:

Right of Substitution/Personal Service

Is there a requirement for the worker's personal service?

Control

Is there a sufficient degree of control over the worker?

Mutuality of Obligation

Are the mutual obligations of the contract consistent with employment?

Why are these three areas so important? Because if the answer to any of these questions is 'no', the contract cannot be an employment, whatever other terms it may contain.

This fundamental approach was originally set out by McKenna J in an employment status dispute between Ready Mixed Concrete (South East) Ltd and the Social Security Minister back in 1968. Since he gave his judgment in the High Court, it has received widespread judicial approval, and has been referred to as the 'safest starting point' when considering employment status.

So what can we derive from this? If a contract does not contain a requirement for personal service or there is insufficient control or there is a lack of mutuality of obligations the contract cannot be a contract of employment. There is no grey area, no weighing up of factors. If any part of this 'irreducible minimum' is missing the contract cannot be a contract of service.

How to Prepare?

Plan

Most contractors will need to assess their current working relationships and contractual terms with their Client (Engager) be that direct with the end client or via a third party.

Most companies will be auditing their contractor workforce to understand roles that fall inside IR35 to evaluate their risk.

Companies shall look to make determinations and enforce a framework agreement with their contractors and third party agency suppliers.

Once these determinations have been completed the need to engage a payroll provider will be important. Understanding how PAYE and Employers NI is deducted, along with pension contributions and employment rights is important.

Make sure you understand these deductions, financially plan accordingly and work with a reputable PAYE provider.

Substitution/Personal Service

In order to remove any requirement for personal service there should be a complete (or not unreasonably restricted) right to substitute personnel, or even to assign or subcontract the services to another party altogether.

For example, if the contract enabled the company to utilise whoever it liked to perform the services, there would not be any requirement for personal service, and this would be inconsistent with an employment relationship.

However, in reality you are unlikely to encounter an unlimited right to substitute, so it is important to be aware of how the law views restrictions on substitution rights.

In the case of McMenamin v Diggles (1991) a barrister's clerk had the right to send a substitute providing the substitute had at least 10 year's experience. This condition was not found to displace the right of substitution. This was affirmed in the later case of Express & Echo v Tanton (1999) where the right to send a substitute was not affected by the condition that the substitute had to be suitably qualified.

Therefore a term which read:

would be acceptable.

If, however, the clause stated that the client had the right to reject a substitute, the client could still demand personal service by rejecting any substitute.

Control

It is perfectly reasonable (and probably typical) in a self employed contract for services that there be a comprehensive job specification which outlines the service that is to be provided, where the service is to be provided and the hours during which it is to be provided. For there to be a contract of employment however, there must be a right of control over how the service is to be provided.

In the case of McManus v Griffiths (1997) a lady who supplied catering services to a golf club was found not to be an employee of the club. The courts found that although she supplied the services on their premises during the times required by the club and used the clubs equipment, the club had no control over the way in which she supplied the services and therefore she could not be an employee.

As an example, a contract which included the term:

would contain an insufficient degree of control to be a contract of employment.

Mutuality of Obligation

This is an area in which the Inland Revenue have been judicially criticised, and one which commonly causes confusion.

Within any contract there are various mutual obligations – the obligation to perform and be paid for performing would form part of any contract – but the mutual obligations needed for a contract of employment to exist consist of more that this.

A lot has been written on the subject of mutuality of obligations in the context of employment but instead of getting tied up in phrases like 'care and continuity' and 'trust and confidence' it is probably safer simply to look at the definition that has come out of the major case law decisions.

In cases such as O'Kelly v Trustehouse Forte (1983) and Carmichael v National Power (1999) the question asked was: is there an obligation to offer and an obligation to accept future work. In both cases the answer was no and therefore the courts found that there was not sufficient mutuality of obligation to form a contract of service.

Therefore, if a contract has a clause which reads:

There can be no mutuality of obligation and therefore no contract of employment.

There are, of course, various other factors which may be taken into account when deciding status such as the intention of the parties and the level of financial risk undertaken, but the point to be remembered is this; if any part of the irreducible minimum is not present, then the relationship simply cannot be one of employer and employee.

Working Outside IR35

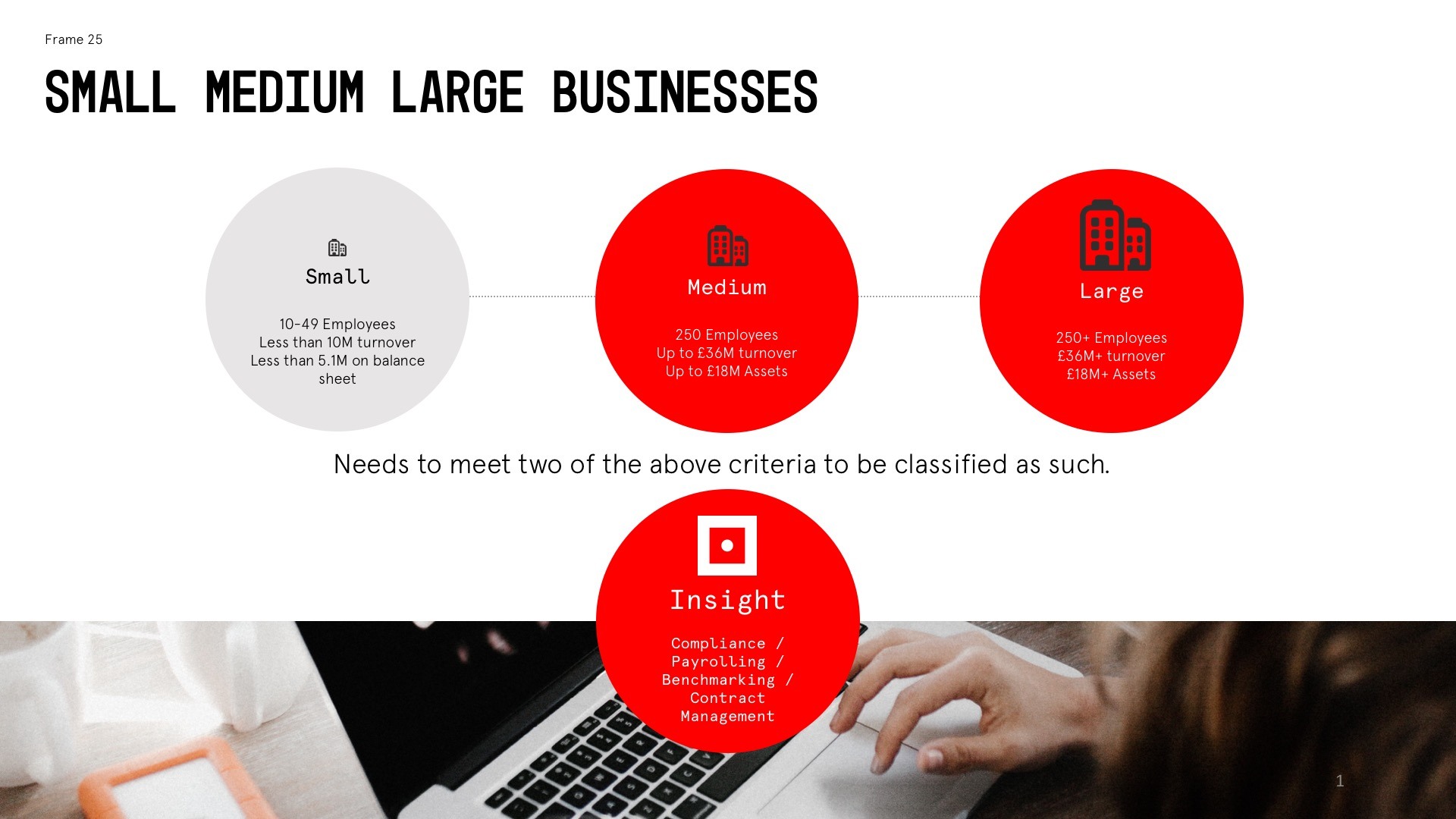

Where the end user of the worker’s services is a small business, it is confirmed that the responsibility for assessing the arrangements and applying IR35, will remain with the PSC. This will be the case even where the worker is provided via a third party such as an agency.

Working Inside IR35

From April 2020, the new legislation will place the burden for determining whether IR35 applies onto the private sector, and the engager of PSC’s if the engager is a medium or large company.

The Engager or End client is responsible for determining IR35 status of the worker (because the end client is best placed to establish employment status based on contract and working practices)

If inside IR35, the Fee Payer pays Income Tax and NICs (employers and employees) to HMRC this is done directly via Pay 25’s PAYE solution.

So what do I do with my Ltd Company?

As an aside, if you fall inside of IR35, your net pay through a Limited Company won’t be too dissimilar to that of an Umbrella Company because the same deductions for tax and NIC contributions must be made regardless. If you do fall inside of IR35, we would recommend using PAY 25 PAYE to process your payments because the additional workload involved in running your own business outweighs the minimal financial gains.

Employers NI

Employers are liable to pay Employers NI - (Employer’s National Insurance Contributions (NICs) for all permanent staff on their payroll.

When working via a third-party payroll provider, Employer NIC is still paid on the workers assignment income. Therefore the rate offered to the worker will be adjusted to reflect this.

It is important to take this into consideration when negotiating pay rates with agencies and end clients. For example if you accepted the same rate when a member of staff you would take home less money due to the Employers NICs being added to the deductions.

Employer’s NIC’s stands at 13.8% only levied on earnings above 156 per week and is uncapped. So not taking into consideration any expense claims this is percentage increase you would need to negotiate in order to ensure the rate was comparable to that of the permanent rate.

Eg.

Permanent Hourly Rate - £25

Contractor Hourly Rate - £28.45

Umbrella Companies

An umbrella company is a PAYE provider and acts as an employer for contractors on temporary contracts, typically working through a recruitment agency.

An Umbrella company acts as an employer for contractors on temporary contracts, typically working through a recruitment agency. It serves as a single employer throughout multiple contracts – contracts are between your clients and the Umbrella company, which pays you as an employee through the PAYE system.

The Difference between an Umbrella and PAY 25

An Umbrella typically charges anything between £15-25 per week to each employee.

PAY 25 is free for employees, we do not charge fees to the worker.

Dangers of Umbrellas

Due to the fact expenses can no longer be claimed, a number of Umbrellas compete to get contractors to sign up by using attractive headlines like - ‘guaranteed 90% take home pay’.

Simply put, this scheme would be tax evasion.

A number of umbrella companies have also used loan schemes to ensure a high net take home for the contractor.

Contractor loan schemes (or, as the Government calls them, disguised remuneration arrangements) take many forms – but the underlying structure is that a freelance or contract worker signs a contract of employment with an employer or EBT (employment benefit trust), usually located outside mainland UK jurisdiction. The employer then pays the contractor in the form of tax-free ‘loans’ – which, although appearing as loans on paper, are never expected to be repaid. In return, the scheme provider takes a percentage of the contractor’s income as an ‘administration fee’.

Since the rise of contractor loan schemes HMRC has taken decisive action against users of such arrangements – retrospective legislation was introduced covering transactions as far back as 1999, levying charges of up to 100% of tax avoided (as calculated by HMRC) on the individuals caught in the net.

We have also seen a number of new schemes that use annuities in a similar way. We would expect HMRC to focus on these in the future.

Why won't an Agency allow me to work via an Umbrella Company I have found online?

This is a common question, and relates to compliance and the criminal finance act

The new Criminal Finances Act was announced in April 2017, and came into force on 30th September. This makes partnerships or limited companies ‘criminally liable’ if they do not prevent their staff, suppliers and clients – or any other ‘external agent’ within the supply chain – from carrying out tax evasion.

Important to note this ‘prevention of tax evasion’ offence can be deemed to have taken place even if the senior management team of the business in question was not involved in, or aware of, the act of tax evasion being carried out.

There are two aspects to the new legislation. Firstly the facilitation of the evasion of UK tax, by any business wherever it is located – and secondly, the facilitation of non-UK tax evasion, by businesses with a UK connection.

HMRC’s aim is to ensure that companies do not ignore the activities of the people they work with, and to make these companies liable for their ‘failure to prevent tax evasion’. If a company is prosecuted and convicted of this offence, there are unlimited penalties which could be applied, so it’s essential that you know exactly how the new legislation works, and that you ensure you are not at risk.

The offence of ‘tax evasion’ itself has not changed, and the same rules apply – when a person or an organisation does something intentionally, which enables them to pay less than their true tax liability, then it is an offence. This means deliberate dishonesty, meaning that a genuine mistake, or even a careless act, would not result in a conviction. These tax evasion laws cover not only personal income tax but also corporation tax, VAT and National Insurance contributions.

Assigning criminal liability

With the new legislation, HMRC has altered the way in which criminal liability is assigned, creating a situation where an ‘associated business’ may be liable for a tax avoidance offence by someone within their supply chain, simply because they were aware of and did nothing to prevent it. It is now much easier for HMRC to convict companies that facilitate tax evasion in some way, even if that is just by not taking full responsibility for ensuring their supply chain is operating in a compliant manner.

This has huge implications for recruitment agencies, which deal with limited company contractors, umbrella companies and contractor accountancy firms. The onus is now on these organisations within the supply chain to ensure that their industry colleagues are not committing, encouraging, or turning a blind eye to tax evasion activity.

What does it mean for recruitment agencies?

As mentioned in the IR35 section there is a long history of tax evading umbrella companies providing loan schemes, annuities and job board schemes. So, while much has been done to eradicate them, no-one operating in this industry can afford to be complacent about the fact that such schemes could still be taking place somewhere within their supply chain.

As an example, an agency would be deemed liable for ‘failing to prevent tax evasion’ if a recruitment consultant encouraged a limited company contractor client to get involved in this type of scheme, when they knew it was set up in order to avoid tax. The agency would also be liable even if an agent was simply aware that a contractor client was involved in this type of scheme, even if they were not involved in encouraging or recommending it. In this situation, a Recruitment Agency would be considered to have ‘failed to prevent the facilitation of tax evasion’.

The only way to avoid criminal liability is to show that the agency has implemented ‘reasonable prevention procedures’.

It is for these reasons why a recruitment agency will typically only work with trusted suppliers, or in our case why we setup Pay 25 to ensure we have visibility and control across our supply chain.